Budget 2026 takes aim at overdrawn shareholder accounts – by Kevin Davies

- May 29

- 7 min read

New rules announced this week will tax outstanding shareholder loans as income six months after a company is removed from the Companies Register. If you are a director, shareholder, or adviser - or if you have a company in financial difficulty - this change matters to you.

Data from 31 March 2024 reveals the scale of the shareholder loan problem that Budget 2026 seeks to address.

Budget 2026 — Key Facts at a Glance

Trigger: Company liquidated or removed from the Companies Register

Timing: Outstanding shareholder loan becomes taxable income 6 months after removal

Revenue: $146 million forecast over the Budget period

Affected persons: Shareholders, directors, and close relatives of a shareholder or director - regardless of whether the borrower is a natural person, trust, or company

A $29 Billion Tax Gap

For decades, overdrawn shareholder current accounts have been a fixture of New Zealand’s small business landscape. A director draws money from the company - perhaps to pay personal bills, fund a lifestyle, or tide over a cash shortfall - and books it as a loan from the company rather than a salary or dividend, with taxes paid. This shareholder loan sits on the balance sheet, interest charges are only sometimes applied, and in many cases it simply grows, year by year, without repayment. Then on liquidation it is all too often not collected.

Inland Revenue has been watching. As at 31 March 2024, 119,000 New Zealand companies were owed nearly $29 billion by natural person or trust shareholders - and that figure has been increasing. Much of this debt will never ever be repaid, and under the rules that existed until 28 May 2026, none of it was taxable as income. Budget 2026 changes that.

What the Budget Announced

New rules will be introduced under which, six months after a company has been liquidated or otherwise removed from the Companies Register, any outstanding loans the company previously made to its shareholders will be taxed as income to those former shareholders. The Government’s stated position is unambiguous:

“Six months after a company has been liquidated, or otherwise removed from the Companies Register, any outstanding loans it previously made to its shareholders will be taxed as income. It is unlikely such a loan will ever be repaid, so is

effectively income to the former shareholder. Not taxing it is unfair to all the other New Zealanders who pay income tax and contribute to the costs of public services.”

This is a targeted but significant measure. It does not (at least at this stage) adopt the broader proposals from Inland Revenue’s December 2025 issues paper, which had proposed treating loans over a $50,000 threshold as income (characterised as deemed dividends) if not repaid within 12 months. What has been enacted is more specific: it targets

the deregistration endpoint - the moment at which, practically speaking, any prospect of repayment disappears. The technical mechanism under the enacted rule is that the remaining payments under the financial arrangement are deemed to be discharged six months after removal from the register. The borrower must then calculate a base price adjustment (BPA) under the financial arrangements rules, and it is that BPA calculation which produces the taxable income. This is distinct from, and should not be confused with, dividend treatment. Importantly, the new rule applies retrospectively to any company removed from the register on or after 4 December 2025 - the date the officials’ Issues Paper was released. This means the clock is already running for some companies removed in the past six months, and the six-month window may be imminent for others.

The scope of the rule is broader than shareholders alone.

The IR information sheet confirms that the rule extends to loans made to a director of the company (not just

shareholder-directors) and to close relatives of a shareholder or director. This prevents the rule being sidestepped by routing the loan through a related party. Conversely, the rule is expressly confined to closely-held companies: widely-held companies, partnerships, and sole traders are expected to be unaffected.

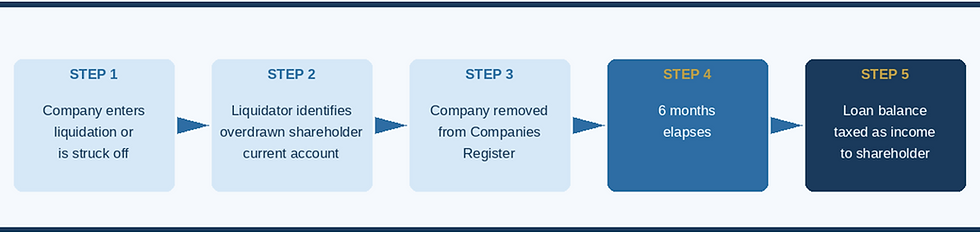

The Liability Pathway: From Liquidation to Income Assessment

The five-step pathway from company liquidation to income tax assessment on the former shareholder.

The insolvency dimension of this change is acute. In the vast majority of company liquidations, the shareholder current account is overdrawn. Directors have drawn funds from the company over many years, often without documenting the arrangements properly, and without any realistic plan for repayment. At the point of liquidation, those funds are recoverable by the liquidator as debts owing to the company - and now, six months after removal from the Companies Register, they will also attract an income tax liability in the hands of the former shareholder.

This creates a compounding problem for directors already in financial difficulty. Consider the typical scenario:

The company enters liquidation, already insolvent.

The liquidator identifies an overdrawn shareholder current account of $350,000, and finds voidable transactions for $200,000 against the director.

The director has no material assets from which to repay either the liquidator or Inland Revenue.

Six months after deregistration, Inland Revenue now treats that $350,000 overdrawn shareholder current account as taxable income to the director (changing directors does not help avoid this liability).

A tax liability - potentially $136,500 at the 39% top rate - crystallises on top of whatever personal liabilities already exist.

For a director who has already lost their business, this is a serious further blow. It is also a significant development for trustees and trust advisers, given the prevalence of family trusts as shareholders in New Zealand closely-held companies. We note that the situation where a Liquidator has recovered money to satisfy all of the overdrawn Shareholder Current Account and distributed this to Inland Revenue within 6 months, then there would be no need to tax

the overdrawn shareholder loan balance as income to the shareholder.

Will Inland Revenue Automatically Assess the Income?

This is the practical question that every director, shareholder and adviser will be asking. The enabling legislation has not yet been enacted - Budget day announcements are policy decisions, and the detailed mechanics will emerge through a taxation bill later this year. However, the following can be said with confidence.

Inland Revenue already holds substantial data on shareholder loan balances from company income tax returns (IR4), financial statements filed with those returns, and annual imputation returns. When a company is removed from the Companies Register, the Registrar notifies Inland Revenue as a matter of course. IR will therefore be aware of deregistrations as they occur, and will be able to cross-reference that information against known loan balances.

One initial mechanism could be a targeted compliance programme: Inland Revenue cross-references deregistration data with shareholder loan balances from filed returns, follows up Liquidators, identifies cases where a material balance remains outstanding six months post- removal, and issues either a notice of proposed adjustment (NOPA) or a direct assessment to the former shareholder. The income tax treatment will need to be returned in the relevant return type - an IR3 for a natural person shareholder, an IR6 for a trust shareholder, or an IR4 for a corporate shareholder.

Over time, as the regime matures, it is plausible that Inland Revenue will migrate toward automatic income inclusion in pre-populated returns for individual shareholders. Data collection when filing IR4 returns may require IRD numbers for shareholders to enable a tax return to be successfully filed. The timing complexity - the income crystallises six months

after deregistration, which may fall mid-income year - will need to be resolved in the amending legislation.

The Broader Picture: Inland Revenue’s Compliance Push

This measure does not sit in isolation. Budget 2026 also allocates a further $15 million per annum to Inland Revenue for debt compliance activities, building on last year’s $35 million increase. This additional investment has contributed to

approximately $3 billion in overdue tax being collected in the year to date. Shareholder current accounts are squarely in the compliance crosshairs. Inland Revenue have been asking me increasingly for reconstruction of shareholder current accounts, even if they are still reluctant to fund as many litigation recovery matters as I would like them to.

Directors and shareholders who have been treating overdrawn current accounts as an indefinite deferral mechanism - or as balances that would quietly disappear on a company wind-up - should take notice. That approach is now, formally, over. I am updating my Statement of Quality Management to change my approach, and encourage fellow licensed insolvency practitioners reading this to do the same. It is imperative Liquidators strive to collect overdrawn Shareholder Current Account balances and on pay these to Inland Revenue, or the shareholder current account balance will be transferred to the shareholder (director or family member) to pay income tax on at their marginal tax rate.

What Should Directors, Shareholders, and Their Families Do Now?

While the amending legislation is yet to be enacted, the policy direction is clear and the revenue estimate ($146 million) confirms this is not a symbolic measure. Practical steps to consider include:

Review the balance of any shareholder current accounts in companies you own or direct, and assess the realistic prospect of repayment.

Where a company is heading toward insolvency or strike-off, obtain specialist advice before that process commences - not after, when it is too late.

Trust advisers and accountants should specifically address this exposure in any review of trust-owned company structures.

Directors engaged in voluntary administration or creditor compromise processes should factor the potential income tax liability into their personal financial position. If a company has already been removed from the Companies Register and six months has not yet elapsed, the window for action - whatever form that might take - is now.

Family members of directors and shareholders should be aware that the rule extends to close relatives who have received loans from the company, not only the director or shareholder themselves. Professional advice should be sought if any such loan is outstanding in a company approaching removal from the register.

In some circumstances, depending on how the legislation is drafted, it could perversely be prudent to not repay the shareholder current account until six months have expired, if the shareholder, director or family member that has a loan balance owing to the company moves to a lower tax rate.

Kevin Davies is a Licensed Insolvency Practitioner (and RITANZ member) who advises directors, shareholders, lenders and creditors across the full spectrum of insolvency and restructuring work.

Comments